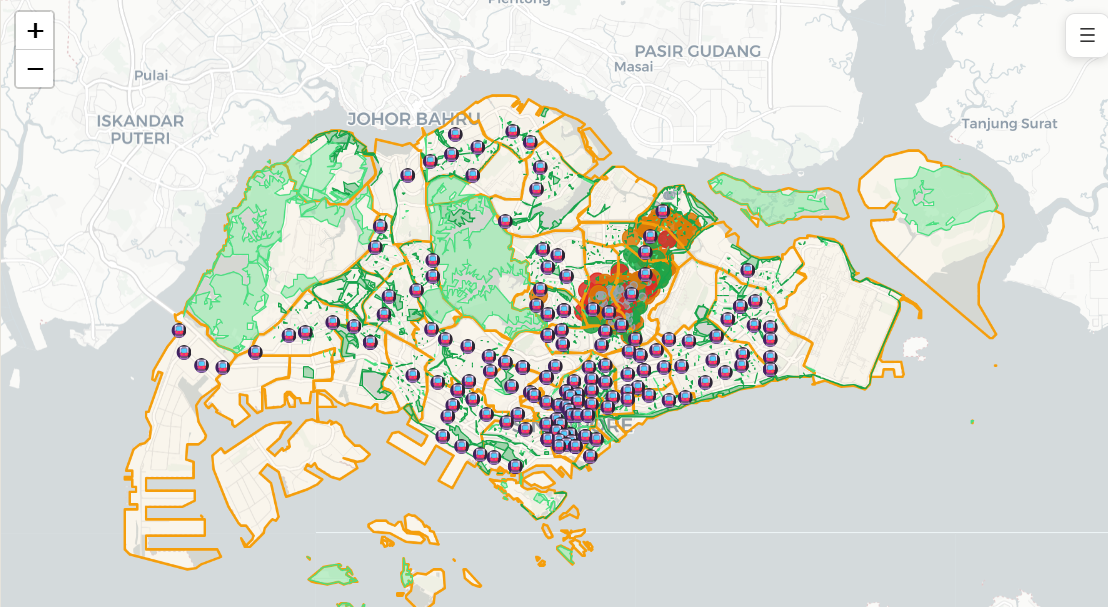

DISTRICT SCREENER

See where the value is

URA zoning. Future MRT corridors, landed housing zones, planned green spaces and more. All in one map. No other property platform in Singapore shows you this.

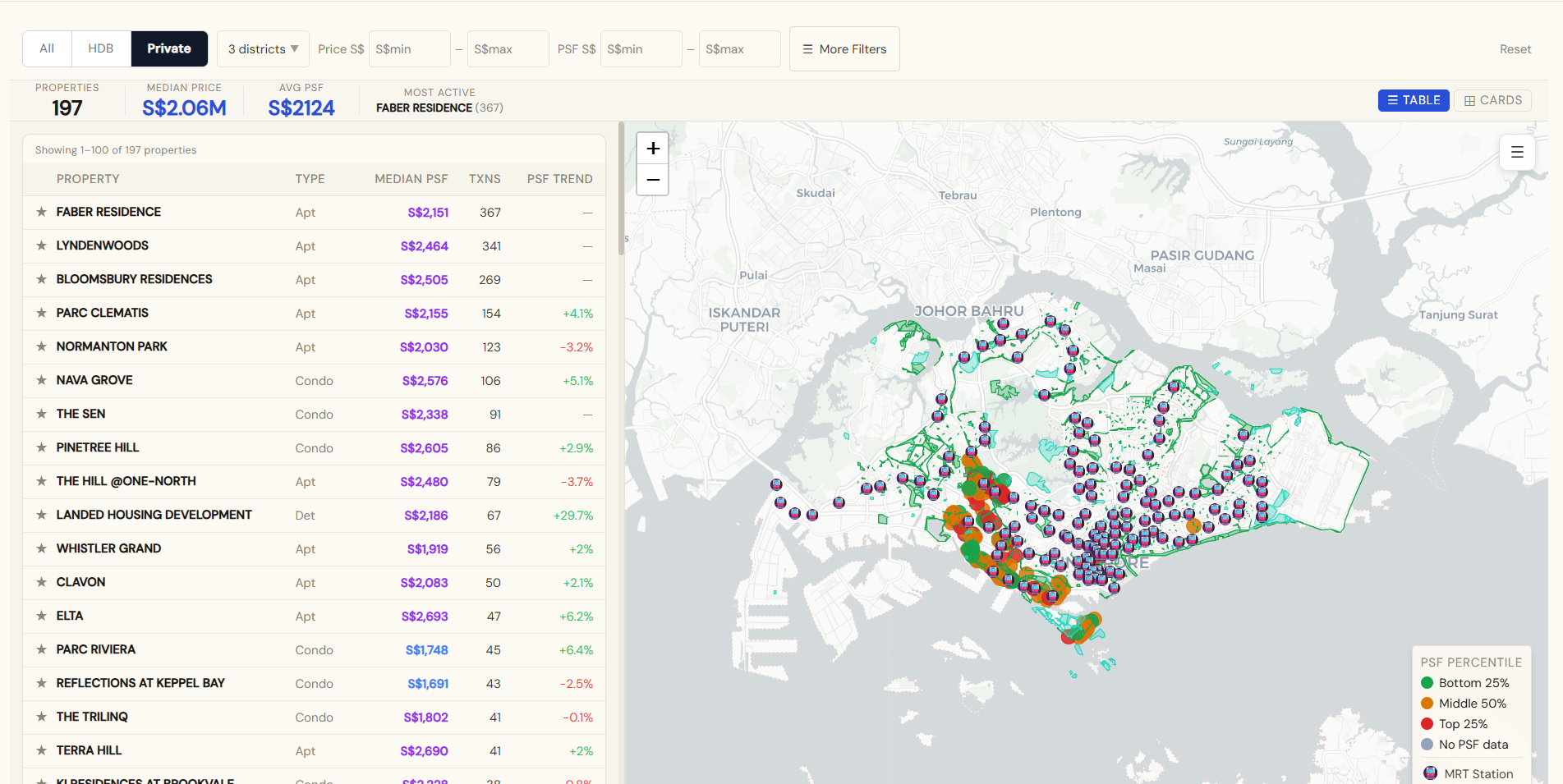

Singapore Property Intelligence

371,000 real transactions. Every HDB block, every condo, every district. We pulled the data, we create the analytics, so you don't have to.

DISTRICT SCREENER

URA zoning. Future MRT corridors, landed housing zones, planned green spaces and more. All in one map. No other property platform in Singapore shows you this.

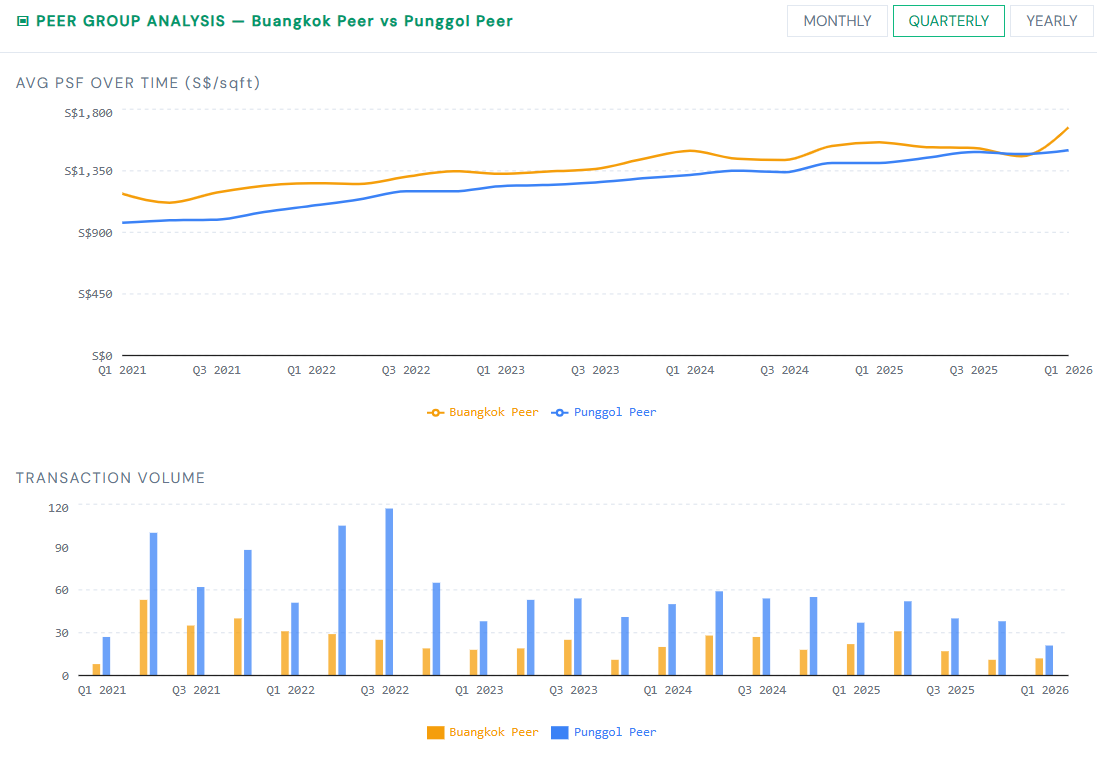

PEER GROUP ANALYSIS

Pick any property. Compare its PSF trend against the neighbourhood over time. See if you're overpaying.

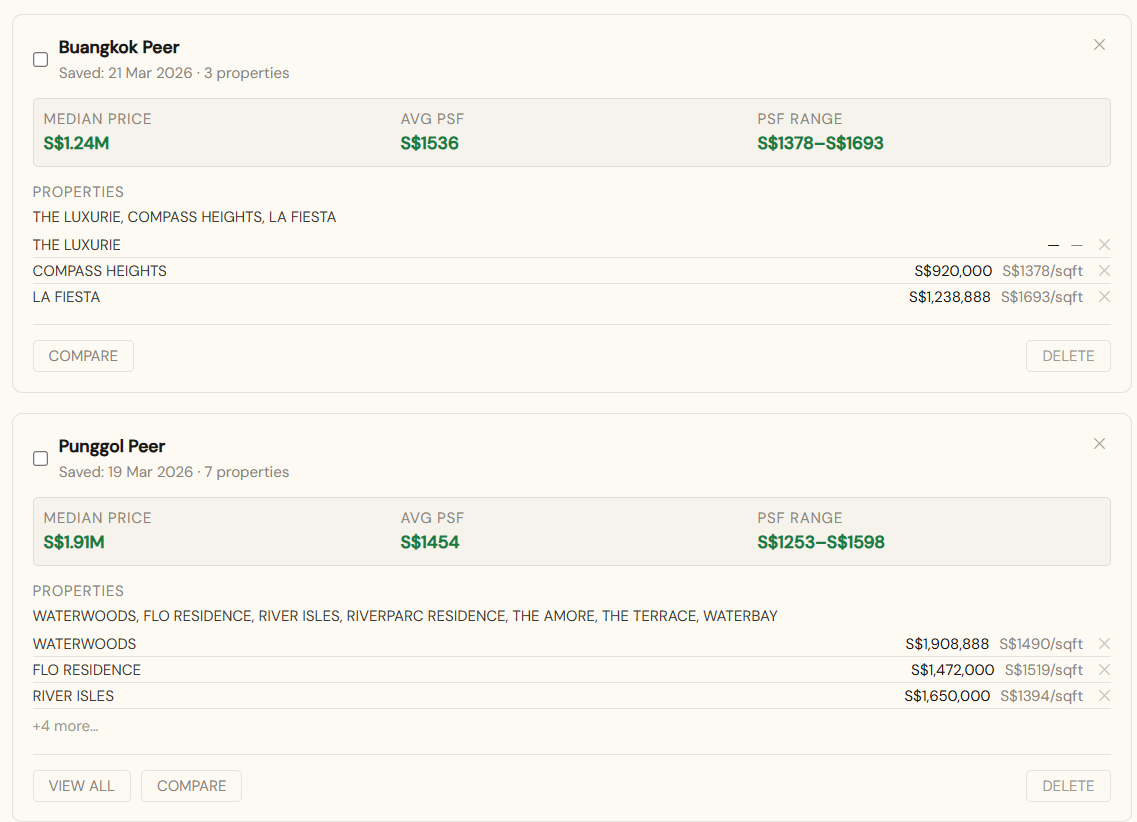

WATCHLIST

Save properties into custom groups. See how they stack up on price, PSF, and recent activity — all in one view.